Here are four of the most common types of equity compensation:

- Incentive Stock Options (ISO). Employees get the right to buy shares of company stock at a set price, known as the strike price, for a period of time. In addition to the potential benefit of buying shares at a discount if the share price rises above the strike price, ISOs also offer potential income tax advantages. However, you will face capital gains tax implications when you sell those shares in the future.

- Non-Qualified Stock Options (NSO). Like ISOs, NSOs give employees the right to buy shares of company stock at a preset price during a certain period of time. The tax treatment of NSOs is different from ISOs, however, in that you must pay income and payroll tax on the difference between the market price and the price you pay for the shares.

- Restricted Stock Units (RSU). RSUs are a promise to award you shares of company stock in the future, but at today’s price. Think of RSUs as similar to a future cash bonus—unlike options, you don’t need to buy the shares first to realize any profit (as long as the stock price has risen since you were granted shares). However, you will owe income and payroll tax on the value of your RSUs.

- Employee Stock Purchase Plans (ESPP). These programs let employees purchase company stock at a discounted price using contributions they make through payroll deductions. The discounted stock price is typically 5%-15% lower than the stock’s market price

Cliff Vesting

Employees receive all granted shares once.

Graded Vesting

Employees receive a percentage or dollar-value of shares over regular intervals.

Hybrid Vesting

A mix of cliff and graded vesting. For example, shares may vest over four years, with 25% vesting after the first year and the rest vesting in equal monthly installments over the next three years..

Vesting example: Let’s say your options grant vests monthly over five years with a one-year “cliff.” This means that you earn the first 20% of shares (i.e., one-fifth) after the one-year mark, and then you earn about 2% monthly for the remaining four years.

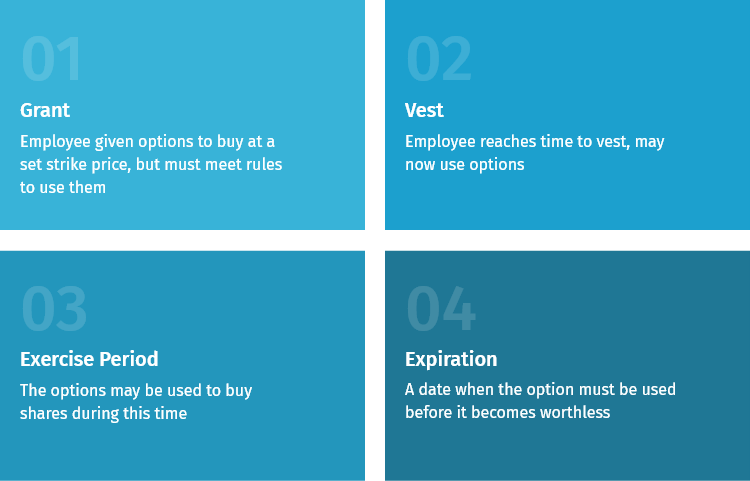

Exercise period

Once you reach the end of the vesting period for ISO/NSO awards, you have a limited window in which to purchase those shares at your preset strike price — known as the exercise period. A typical exercise period is 10 years after the original grant date.

Expiration date

You must purchase all vested options within the exercise period, after which they expire and become worthless. If you leave a company with vested but unexercised options, they typically expire in 60 or 90 days.

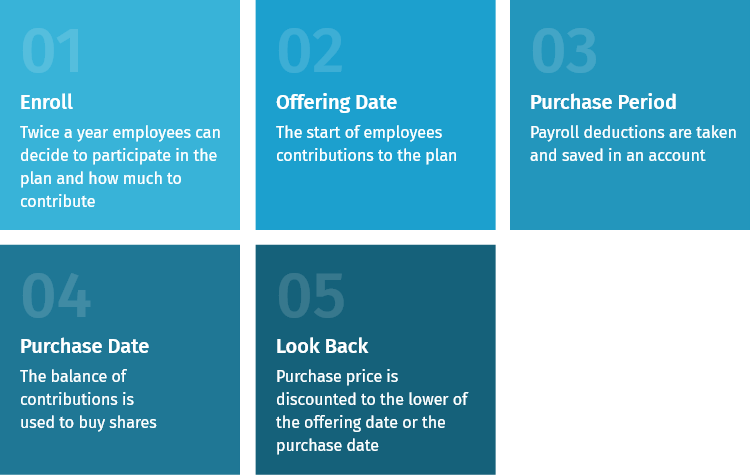

ESPP enrollment and purchase period

ESPP plans have time-based restrictions that determine when you can participate in the plan. First, there’s the enrollment period, which typically takes place twice per year. Once you enroll, you decide how much you’ll contribute from each paycheck beginning at the next offering date.

At the end of a purchase period (often six months), you reach a purchase date, when the money you contributed is used to buy company shares at a discounted price.

ESPP enrollment and purchase example

Alex enrolls in her company ESPP during the November enrollment period. The company starts taking payroll deductions on a December 1 offering date. It purchases shares for Alex on June 15, using the accumulated cash from the December 1 – May 31 purchase period. Alex’s company automatically re-enrolls her for the next cycle, taking payroll deductions for the June 1 – November 30 purchase period.

Performance-based restrictions

Performance restrictions put limitations on when, or even if, you have access to your equity compensation. As with cash bonuses, companies may tie equity awards to revenue growth, profits, or share price goals. At the same time, the company may require an employee to complete education or training or hit personal targets for sales or other criteria before receiving shares.

Limits on sales and use

Shares received through equity compensation may come with further restrictions, particularly if you work for a private company. Transfer and resale restrictions may limit when or to whom you can sell stock. Some companies limit pledging, which is the use of stock as collateral for a loan.

Here are tax considerations to help maximize the value of your options, RSUs, or ESPP awards:

Incentive stock options

One of the advantages of ISOs is that you don’t owe income and payroll taxes when you exercise — as long as you hold those shares for at least two years from the grant date and one year after the exercise date. (If you sell before one year, the difference between the market value of the shares and the strike price will be taxed as ordinary income.)

However, ISOs are not exactly tax-free. The difference between what you pay for the shares and the stock’s fair market value counts towards your alternative minimum taxable income (AMTI).

.png?width=750&name=incentive-stock-options-example%20(1).png)

When you sell the shares, you’ll face capital gains taxes on the difference between the strike price and the sale price. The gain or loss will be measured from your exercise cost — even if you’ve already paid AMT.

Nonqualified stock options

When you exercise NSOs, you owe income tax and payroll taxes (Social Security and Medicare) on the difference between what you paid for the shares (your strike price) and their current market value.

Again, let’s say you exercise 1,000 options at a strike price of $35 per share, and the stock’s current price is $47. You would be taxed on $12,000 of income ($47,000 - $35,000).

Your company may automatically withhold the mandatory minimum 22% for federal taxes, as well as any state minimum withholding, but there’s a good chance your actual tax rate is much higher. It’s important to run a tax projection when planning to exercise options so you don’t face a big tax bill when you file your return for that year.

Once you exercise NSOs, you can sell or hold those shares. When you do sell, any capital gain or loss will be measured from the shares’ fair market value on the date of exercise. If you hold those shares for at least one year after your exercise date, you’ll qualify for the long-term capital gains rate on any increase in value.

Restricted Stock Units

With restricted stock units, there are no taxes at the time of grant since the shares are not technically yours yet. But, in the year your RSUs vest, their share value is considered ordinary income, and you are taxed just as if you had received the same amount in cash. Even if you don’t sell them, the share value is subject to federal, payroll and applicable state and local taxes for that year.

After that, any change in value from the vesting price is taxed as a capital gain or loss when you sell the shares. If you vest and then immediately sell your shares, it stands to reason that you incur neither a gain nor a loss.

Employee Stock Purchase Plans

With an ESPP you only incur taxes when you sell the shares, not when you purchase them. The less-good news is that ESPP tax planning is complicated by “qualifying” vs. “disqualifying” dispositions.

A disqualifying position (selling right away)

Selling ESPP shares held for less than two years after the offering date or less than one year after the purchase date is a disqualifying disposition. In a disqualifying disposition, any gains in the shares are taxed at (typically higher) ordinary income tax rates.

A qualifying position (selling after a waiting period)

ESPP shares are eligible for preferential tax treatment under a qualifying disposition. To make a qualifying disposition, shares must be held for at least two years after the offering date, and at least one year after the purchase date.

A qualifying disposition allows gains above the discount to be taxed at (typically lower) long-term capital gains rates. The company discount is always taxed as ordinary income.

Tax smart strategies - Common mistakes to avoid

The complex tax rules that govern equity compensation can sometimes result in people making costly missteps. Before you take action with newly acquired company shares, it’s important to develop a strategy for what you will hold and what you will sell.

Here are three common tax mistakes to watch out for:

1. Holding RSUs longer than necessary

Employees often get confused about the holding periods required for different kinds of equity compensation. For RSUs there are no tax advantages to holding the shares after they vest. In fact, selling them at the time of vesting limits potential appreciation, which may make it a tax-efficient time to sell.

2. Selling ISOs and ESPP shares too soon

The long-term capital gains tax rates are the lowest available tax rates for stock options and ESPP shares. You should consider hanging onto ISO/ESPP shares for at least two years from the grant date and one year after you take possession of the shares to qualify for those rates.

3. Selling shares without a tax strategy

Although you may face a significant tax bill when you sell company shares, you can manage those costs if you develop a good strategy in advance. For instance, you can time your sales to spread the tax bill over different tax years, or focus your sales on years when your tax bracket might be lower. An advisor may be able to help you identify other assets that have suffered losses to sell, so you can take advantage of tax-loss harvesting to offset taxes on your equity compensation shares. You might also use other strategies, like selling during market dips or making a charitable gift of appreciated securities.

Download a PDF of this Guide

Enter your information below to receive a PDF copy of this Equity Compensation guide.

Disclosure

For informational purposes only; should not be used as investment tax, legal or accounting advice. Plancorp LLC is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training nor does it imply endorsement by the SEC. All investing involves risk, including the loss of principal. Past performance does not guarantee future results. Plancorp's marketing material should not be construed by any existing or prospective client as a guarantee that they will experience a certain level of results if they engage our services, and may include lists or rankings published by magazines and other sources which are generally based exclusively on information prepared and submitted by the recognized advisor. Plancorp is a registered trademark of Plancorp LLC, registered in the U.S. Patent and Trademark Office.

![]()

![]()