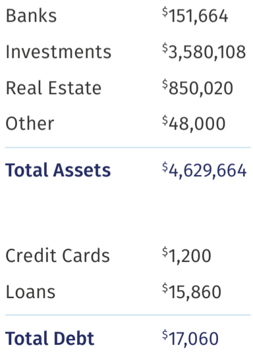

Calculating Your Net Wealth

Your Personal Wealth

When you build a mock budget, estimate on the high side for expenses and spending.

A majority of people believe that their annual spending during retirement will be 70% to 80% of their past expenditures, but that often isn’t the case.

For more information, you can visit Medicare.gov -- but know it’s easy to get lost in the Medicare maze. Start by prioritizing the elements of Medicare insurance coverage you think are most important. You can even try categorizing different features by affordability, flexibility, cost certainty, and worst-case protection.

Finally, it’s important to think about the tax impact of your withdrawal strategy. As you think about when to tap your various accounts for retirement income, managing retirement income to the best possible tax scenario can be extremely complicated without guidance.

.png?width=600&height=600&name=Untitled%20design%20(1).png)

What Type of Debt Do You Have?

If you have consumer debt, prioritize paying it off now. Start with high-interest debt, like credit card balances, personal loans, or mortgages. But don’t use a lump-sum withdrawal from your retirement accounts to pay it off—the taxes you’ll pay will likely be higher than any interest savings.

If you still have a home mortgage, consider refinancing before you retire to reduce the interest burden over the life of the loan. But don’t forget about closing costs – these can reduce how much money you actually save, or could extend the point at which you would need to stay in your home to hit the break-even mark.

Should You Refinance?

To evaluate whether refinancing makes sense, a good rule of thumb is to divide your closing costs by the monthly savings. If the answer is 24 or less, refinancing usually makes sense.

If your personal balance sheet is in rock-solid shape and you’re still earning an income, but you don’t have any emergency savings, you may even consider a cash-out refinancing to access some of the equity you’ve built up in your home.

When interest rates are low, you may also be at an advantage. But there are hidden costs (think: appraisal, loan origination fees, recording fees, taxes, and more) to be aware of with refinancing, so make sure the numbers make sense before you take a trip to the bank. If you’re not able to commit to keeping high-rate debt like a mortgage under control, this may not be a good fit for you.

4 Reasons to Refinance

.png?width=746&name=4%20Reasons%20to%20Refinance%20%20(1).png)

Also, if you can’t refinance your home for any reason, you still have options like a loan modification or, depending on your age or current situation, an intrafamily loan.

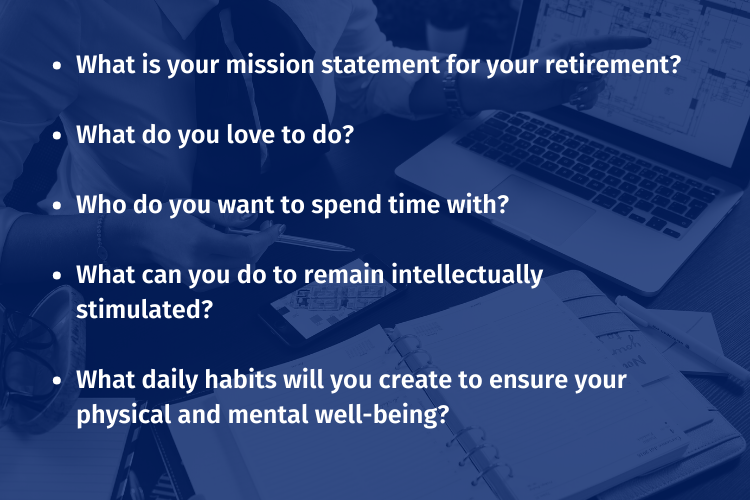

Great Questions to Start With

Asking yourself questions like these can prompt the kind of information that would be good to include on a retirement life plan so you feel not just financially prepared, but mentally and emotionally, too.

The following is a list of items to consider if you are five to 10 years away from retirement.

If you don’t have the time, interest or knowledge to complete these items, consider hiring a CFP® to help.

Download the PDF Version

If you like the above content you can download PDF version of it here.

Disclosure

For informational purposes only; should not be used as investment tax, legal or accounting advice. Plancorp LLC is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training nor does it imply endorsement by the SEC. All investing involves risk, including the loss of principal. Past performance does not guarantee future results. Plancorp's marketing material should not be construed by any existing or prospective client as a guarantee that they will experience a certain level of results if they engage our services, and may include lists or rankings published by magazines and other sources which are generally based exclusively on information prepared and submitted by the recognized advisor. Plancorp is a registered trademark of Plancorp LLC, registered in the U.S. Patent and Trademark Office.

![]()

![]()