Smart investment decisions are necessary on the road to financial security, but it's important to understand how to analyze the risks and returns associated with investment decisions. Knowing how to analyze risk and return properly can help you build a successful portfolio.

In this article, you will get a good idea of how to analyze risk and return in investing.

What Is Risk and Return?

Given a choice between two investment portfolios with identical rates of return, it's important to consider the potential for risk when making an investment decision.

You can quantify uncertainty or risk by looking at the standard deviation of returns — a higher standard deviation indicates a higher level of volatility, or greater uncertainty, in your expected return. This principle is illustrated by comparing two portfolios with the same average return but different volatility levels.

However, this isn't perfectly applicable in real-world situations, where investors typically want to compare a range of portfolios with various returns.

Depending on their situation or financial goals, individual investors may pepper their portfolios with assets such as single stocks, mutual funds, treasury bills, corporate bonds, or savings accounts. You may have been given individual stock as part of your compensation or bonds from a family member.

It pays to be aware of the types of risk associated with each asset class — for instance, market risk, liquidity risk, and time frame — and to ensure that returns are in line with the risk level you're comfortable with.

This is why a diversified portfolio with a mix of low-risk, low-return, and high-return assets is often recommended. After all, diversification is a core principle in investing for a reason.

Long-term investment strategies can further reduce volatility and the risk of loss of principal over a particular time period. Ultimately, investors should evaluate the expected return of each investment and its associated risks before committing to it as a way to meet their unique financial goals.

Risk and Return of a Portfolio

Risk and return are both expressed as a percentage of the value of the portfolio. The risk of a portfolio is its potential to lose capital. When a portfolio has high risk, its potential return is also high. Risk and return are not directly correlated, but they are related.

What is the Risk-Return Tradeoff with Investing?

The risk-return trade-off in investing is a concept that encapsulates the idea that investing is about balancing risk and reward.

In general, the higher the risk associated with an investment, the higher the potential return.

Knowing this, a well-balanced portfolio will include a variety of investments with different levels of risk to maximize the potential return while managing the risk taken.

Utilizing the Sharpe Ratio to Compare Portfolios on a Risk-Adjusted Basis

The Sharpe ratio allows a comparison of portfolios on a like-for-like basis by taking into account the risk level associated with each portfolio.

The Sharpe ratio measures a portfolio's risk-adjusted return or the amount of additional return generated per unit of risk.

It helps to understand the risk-return trade-off, whereby a portfolio with higher returns can only be considered an advantageous investment if the additional risk is not so great it outweighs the benefit. A higher Sharpe ratio indicates a better risk-return trade-off.

Risk Return Tradeoff Example

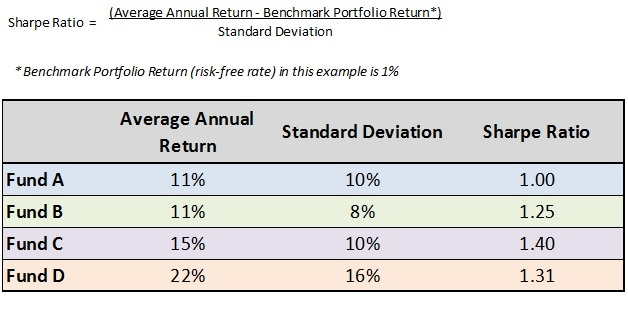

Let's look at an example. Below is the Sharpe ratio equation, followed by a table showing four funds with different returns and standard deviations. In this example, the Sharpe ratio is used to identify the fund with the best risk-adjusted returns:

Fund A and Fund B have identical returns, so you know to choose the fund with lower volatility, which is Fund B. You would expect Fund B to have a higher Sharpe ratio because it has a higher return and lower volatility (standard deviation). Fund B has a higher risk-adjusted return and is therefore preferred over Fund A.

Now let's compare Fund B and Fund C. Fund C offers a higher return than Fund B, but it's also more volatile. This is the perfect scenario to use the Sharpe ratio. Remember, a higher Sharpe ratio is better and indicates a higher risk-adjusted return. Fund B has a Sharpe ratio of 1.25, and Fund C has a Sharpe ratio of 1.40, which means that Fund C has a higher risk-adjusted return than Fund B.

Finally, Fund D has the highest return and volatility of the four options. Using the Sharpe ratio, you can see that Fund D has a higher risk-adjusted return than Fund A and Fund B. However, the compensation for the additional risk assumed in Fund D is not as great as in Fund C. Therefore, the Sharpe ratio indicates that Fund C offers the highest risk-adjusted return and is the best investment option.

The Sharpe ratio is one of many tools we use internally to evaluate investment funds, strategies, and asset classes in client portfolios. A variation of the above ratio is to use a different benchmark portfolio, such as an index (e.g., S&P 500, Russell 2000, MSCI EAFE, etc.), instead of the risk-free rate.

However, this is less useful when comparing investments across different asset classes. Another related tool you can use is the Sortino ratio, which focuses specifically on downside volatility.

Understanding the Relationship Between Risk and Return

When deciding between portfolios with identical returns, an investor should choose the least risky portfolio. Since it's rare for all portfolios to have exactly the same returns, the goal is to achieve the best risk-adjusted return. Volatility is the cost of higher returns, and the Sharpe ratio helps ensure you get the most bang for your buck in a more predictable manner.

The next piece of the puzzle is understanding your personal risk tolerance. Even if a high-risk investment generates enough return to justify the volatility, some investors are unable or unwilling to take that risk. You may be nearing retirement, need reliable access to liquid cash in the near future, or generally not be willing to cope with downswings in the market. The goal at Plancorp is to create a portfolio with a level of risk that will generate enough profit to allow you to sleep at night.

Are you making the right decisions with your money? Plancorp's financial analysis will help you identify areas to focus on and gain personalized suggestions based on your responses.

Disclosure:

This material has been prepared for informational purposes only and should not be used as investment, tax, legal or accounting advice. All investing involves risk. Past performance is no guarantee of future results. Diversification does not ensure a profit or guarantee against a loss. You should consult your own tax, legal and accounting advisors.

-Jun-15-2026-01-48-58-9443-PM.png?width=266&name=Copy%20of%20blog%20featured%20image%20(1)-Jun-15-2026-01-48-58-9443-PM.png)