It’s common knowledge that simply saving for retirement isn’t enough. Investing those savings can help your nest egg outpace inflation and grow exponentially to maximize your retirement potential.

But if your portfolio isn’t structured to minimize your tax burden, you could end up paying the IRS more than you need to, reducing investment gains and jeopardizing your ability to achieve your long-term financial goals.

A tax-efficient portfolio helps increase your net investment income and protects future wealth by reducing the amount of taxes you must pay.

Here's a brief example that shows the benefits of holding investments in the optimal asset location.

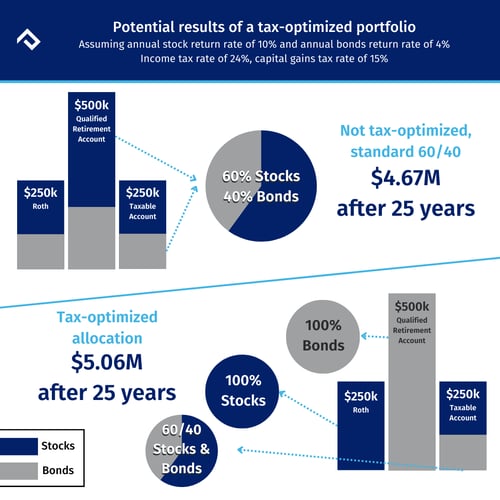

Let’s say you have a $1M portfolio with $250,000 invested in a Roth, $500,000 in a qualified retirement account and $250,000 in a taxable account.

Stocks earn an average annual return of 10%, bonds earn 4%, your ordinary income tax rate is 24%, and your capital gains tax rate is 15%.

If your portfolio is equally weighted so each account has an allocation of 60% stocks and 40% bonds, you’ll have an after-tax investment portfolio of approximately $4.67M after 25 years.

Now, let’s say you optimize your portfolio, so the Roth is invested in 100% stocks, the qualified account is invested in 100% bonds, and the taxable account is invested in 60% stocks and 40% bonds.

You’ll have an after-tax investment portfolio of approximately $5.06M after 25 years. That’s a difference of almost $400,000.

This exact allocation may not make sense for everyone's portfolio, but is an example of the power of optimizing the location of assets across your portfolio and the impact it can have on your after-tax returns over a long period of time.

Here’s a closer look at what a tax-advantaged investment portfolio is, ways to structure one, and how it can benefit you now and in the future.

What is a Tax-Advantaged Investment Portfolio?

A tax-advantaged investment portfolio seeks to reduce the amount of money you pay in taxes while preserving your ability to meet your financial goals — whether that’s leaving an inheritance to your kids or passing a portion of your estate to your favorite charity.

Tax-efficient portfolios place assets in the most optimal location to give you the best chance of increasing your after-tax investment returns.

When you optimize your investments for tax efficiency, it helps you decide — from a tax perspective — what assets are best to use during your lifetime and which are better to leave to future generations or charitable organizations.

How are Investment Accounts Taxed?

Different types of investment accounts are subject to different tax treatments. Here’s a brief overview of the taxes you can expect to pay on qualified, non-qualified and Roth accounts.

Traditional Retirement Accounts

When you contribute to qualified retirement accounts, such as 401(k)s, 403(b)s and traditional IRAs, you receive a tax break in the year you make the contribution.

For example, if you contribute $10,000 to a traditional 401(k), you get a tax deduction of $10,000 for the year. Your contributions grow tax-deferred.

But when you take money out of the account, it’s taxed at your ordinary income tax rate at the time of the withdrawal — which may, or may not, be lower than your tax rate when you were employed.

Roth Retirement Accounts

A Roth account, whether it’s a Roth IRA or Roth 401(k), is the most tax-advantaged account available. You won’t receive a tax benefit when you contribute to a Roth (meaning you can’t deduct contributions for current-year tax liability), but all contributions grow tax-free, and you don’t pay taxes when you make a withdrawal in retirement (after age 59.5).

However, individuals with an adjusted gross income (AGI) of more than $161,000 and couples with an AGI of more than $240,000 aren’t eligible to contribute to a Roth IRA in tax year 2024.

There are no income limitations for Roth 401(k) contributions. However, making contributions to a Roth account instead of a qualified retirement account will increase your tax liability for the current year and you pay taxes at your current tax rate.

It's important to consider if you think your current tax bracket will be higher or lower than it will be in retirement. If you think your tax rate will increase, it generally mean you should pay taxes now and make Roth contributions.

Taxable Non-Retirement Accounts

When you contribute to a taxable brokerage account, you use after-tax dollars. Interest is taxed at your ordinary income tax rate.

Investments that generate dividends are taxed at the long-term capital gains rate — if the dividends are qualified. Non-qualified dividends are taxed at the short-term capital gains rate.

The short-term rate is the same as your ordinary income tax rate and is typically much higher than the long-term capital gain tax rate.

How a Tax-Advantaged Investment Portfolio is Built

Taxes may not be your primary focus when making investment decisions to create a balanced portfolio. But you shouldn’t ignore them because your tax liability can significantly affect your after-tax investment returns.

Structuring a portfolio for tax optimization can reduce your tax bill and increase the amount of money you get to spend in retirement. But investing for tax efficiency requires a personalized approach based on your age, tax bracket, risk tolerance and other factors.

Here are some general principles for allocating investments in the most tax-efficient way based on tax bracket and asset location.

Investors in a Higher Tax Bracket

Municipal bonds are exempt from federal taxes and some state and local taxes as well. They generally have lower expected returns than taxable bonds, but investors in higher tax brackets often earn a higher after-tax return with municipal bonds because of their tax-exempt status.

Investors in a Lower Tax Bracket

Taxable bonds generally have higher expected returns than tax-exempt bonds but are subject to federal and state income taxes. However, they are often a good option for investors in lower tax brackets because they will keep more of the higher expected return due to their lower tax rate, which can often lead to a higher after-tax return overall.

Tax-Optimized Asset Locations

The type of investment you choose isn’t the only factor affecting the taxes you pay. The location of your investments also affects the tax treatment of your assets.

Investments with the highest expected returns, such as stocks, are best held in Roth accounts where they can grow tax-free. Inversely, assets with a lower expected return, such as fixed-income investments, are better in traditional, pre-tax accounts.

Although the future appreciation of these assets is taxable, the goal is to offset your tax bill with shifting more growth over time into the Roth. You also want to hold your most tax-inefficient investments in qualified accounts since taxes are deferred—it's common to hold Real Estate Investment Trusts (REITs), for example.

Taxable accounts are a good place for investments with higher growth potential because gains on investments you hold for more than a year are taxed at the long-term capital gains rate, but if sold within a year, you would be subject to the higher short term capital gains rate, which is the same as your ordinary income tax rate.

Taxable accounts are also an ideal spot for your most tax-efficient assets since you’re taxed on the income your taxable accounts generate each year.

Working with a professional can help you use these best practices to your advantage based on your individual financial circumstances and investment goals.

Tax Strategies for Short-Term Investment Accounts

Investing in the market on a short-term basis is risky. Because the market can be down in any given year, if you invest money you need for the short-term, and the value of your portfolio declines, you may not have enough to cover your expenses. You should keep any cash for significant expenses in the next 12-24 months out of the market, given the uncertainty.

If you have a slightly longer timeline (e.g., 5 to 10 years), you may be able to take on a little more risk. But even over that amount of time, there’s no guarantee your portfolio will have a positive return.

Depending on your risk tolerance, you may consider a more conservative stock-to-bond mix than what you’d choose to fund your retirement account. And if you need the money before turning 59 ½, don’t put it in an account that penalizes you for taking withdrawals before that time.

Tax Strategies for Long-Term Investment Accounts

When it comes to creating a tax-efficient portfolio for the long term, you should optimize what makes the most sense based on your financial goals.

- Choose the appropriate asset location. Because different accounts have different tax treatments, it doesn’t make sense to hold the same types of investments in every account in your portfolio. In general, it’s best to hold assets with the greatest expected returns in Roth accounts and assets with lower expected returns in traditional accounts. Taxable accounts are a good place for higher-growth investments and more tax-efficient assets.

- Maintain multiple account types. Having a combination of tax-deferred, Roth and taxable accounts allows you to withdraw retirement funds in the most tax-efficient way possible throughout retirement.

- Buy and hold. Investments held in taxable accounts for more than a year are subject to the long-term capital gains tax rate, which is preferential to the short-term rate.

- Harvest losses. Tax-loss harvesting when the markets decline can help you stay diversified, disciplined, and help compile tax losses to offset future investment capital gains and reduce your tax bill.

Signs Your Investment Portfolio Isn’t Tax-Optimized

Sometimes, a larger-than-normal tax bill is unavoidable. But it’s worth a look to see if there are things you can do differently to reduce your tax liability in the future. Here are four signs your portfolio may not be tax-optimized.

- You’re not harvesting your losses. Tax-loss harvesting, especially in a down market, can help offset investment gains, resulting in tax savings.

- You’re not following the principles of tax-optimized asset location. Different types of investments receive different tax treatments. Placing them in the optimal type of account can help reduce your tax bill—both long-term and short-term.

- You’re not invested in exchange-traded funds (ETFs). ETFs don’t distribute much, if any, capital gains each year like mutual funds do. Therefore, investing in ETFs helps you minimize the “forced” tax bill you have to pay and gives you more control over the gains you generate and pay taxes on.

- You’re invested in the wrong mutual funds. Mutual funds must distribute capital gains at the end of the year based on how much gain was generated inside the fund itself, leaving shareholders with a pro-rata share of the tax bill. Actively traded mutual funds generate more capital gains you must pay taxes on. Choose funds that take a more passive approach to minimize your tax liability.

Benefits of a Tax-Advantaged Investment Portfolio

The benefits of a tax-advantaged investment portfolio compound over time. When you pay less in taxes, you can keep more money in the market, earning interest year-over-year.

A tax-advantaged portfolio also provides tax diversification in retirement. With multiple buckets of money to choose from, your financial advisor can run projections to determine the best way to take withdrawals to generate the lowest possible tax bill.

How Plancorp Can Help Build a Tax-Optimized Strategy for You

No one wants to pay more in taxes than they have to. But optimizing your portfolio for short-term tax savings could leave you exposed to higher tax liability in the future, particularly in retirement.

That’s why at Plancorp, we help our clients build a long-term tax strategy designed to reduce their lifetime tax burden — not just their next tax bill.

Optimizing your portfolio for tax efficiency now and in the future can help maximize your net investment income over the long-term and preserve future wealth.

Schedule a discovery call for a review of your current portfolio today.

-Jul-20-2026-02-09-55-3575-PM.png?width=266&name=Copy%20of%20blog%20featured%20image%20(1)-Jul-20-2026-02-09-55-3575-PM.png)