Financial planning starts with assessing where you are financially, pinpointing your ideal future state, and figuring out what milestones you need to reach to get there. You need to consider your savings, debts, benefits, investments, and anything else that could impact your financial state now or in the future, but you can't stop there.

Some talk about a financial plan as if it is a simple one-page document that you put together once and never need again. The reality is your financial plan is not a static document — just as your life changes, so too may your financial plan.

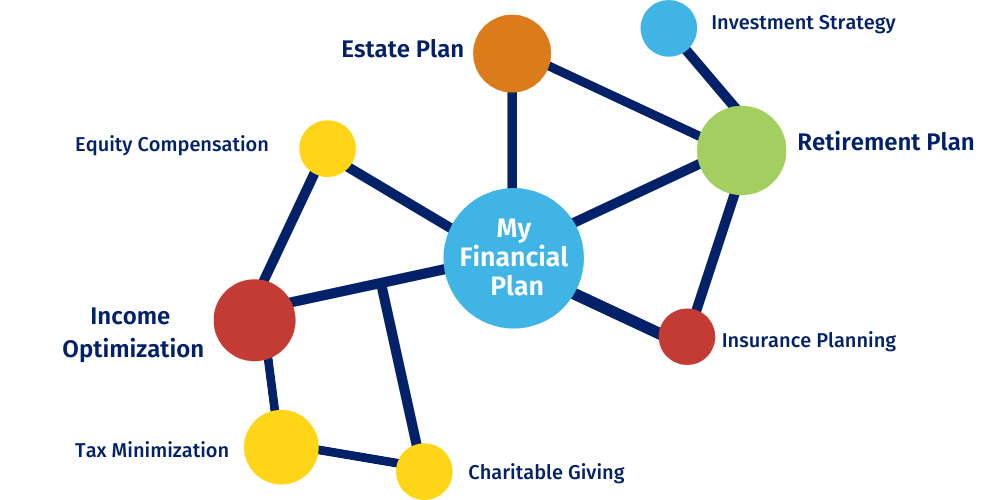

Along with unexpected detours or pivots, positive changes like career progression and starting a family are things your plan needs to take into account. All of these factors are related.

Your employee benefits may impact how you tax-optimize your income and what savings rate you can withstand. Your savings rate will influence your investment strategy and therefor your retirement plan, and so on and so forth.

In short, these are all inter-dependent factors that a simple one-time plan can miss. In fact, some will sell you a 'plan' but in reality it's a financial statement. It outlines what you have and where, but it's not actionable or able to help you make more complex decisions. For that, you'll want to create something with an advisor who can bring it to life.

Working with a good partner ensures your plan is comprehensive, appropriately matrixed, and regularly reviewed, increasing it's resiliency and therefore the likelihood you're able to do what you want with that wealth.

A point of clarification if this is sounding overwhelming: having a solid financial plan does not mean you’re planning every last detail of your life.

You can't predict the future, but a good financial plan can be used as a guide while making decisions to build confidence you aren't inadvertently putting big goals like retirement at risk while dealing with a short-term issue. A great financial plan does that while also helping you make the most of every opportunity along the way.

A great advisor will use the following to help you answer big financial questions with a bit more confidence:

- Knowledge of things like investments, tax strategy, insurance, estate planning, and more. Ideally, they’ll be certified in their understanding of financial planning with a CERTIFIED FINANCIAL PLANNER (CFP®) designation.

- Data, not just on individual pieces of your plan like investment performance, but a comprehensive look at the likelihood you’ll be able to achieve your goals given what we know today, typically in the form of a financial independence analysis.

- Context from their experience with other clients and colleagues, working with your other professional service teams (CPA, Attorney, etc.), knowing who your stakeholders are, and larger market and economic trends.

- A deep understanding of your goals, preferences and vision for life. This is the key to moving from cookie cutter advice that AI could deliver to a truly bespoke plan that leaves your mind at ease.

Family Financial Planning

When starting a family, you need to incorporate these new factors into your plan. As they grow and get established, you'll also want to prepare for expenses like education so you can confidently support them without risking long-term goals like retirement.

Related Reading: Preserving Generational Wealth: What to Know About Family Trusts

Marriage

Starting life with your new partner involves financial decisions, from combining assets to combining bank accounts, signing prenups, and more. Don't let financial stress erode your stability, working with an advisor can build alignment.

Related Reading: How Does a Prenup Work and Should You Get One?

Estate Planning

How confident are you everything is in place to carry out your wishes? Make a plan for assets, investments, savings, and more in your estate plan. A financial planner can help you make sure all the pieces are in place.

Generational Wealth

Maintain family-owned businesses, develop financial literacy, and generate passive income for future family members through investments. Make the right steps to establishing generational wealth today.

Related Reading: How to Build Generational Wealth

Succession Planning

Are you a business owner? Ensure your business is in good hands and step away on your terms with a succession planning advisor. We’ll create an exit plan together that provides the best outcome for you and your business.

Related Reading: The Information You Need For Every Type of Succession Plan

Retirement Planning

Retirement is likely the largest goal incorporated in every financial plan. Saving money isn’t enough — a financial advisor can guide you on the path to saving and investing enough to make your retirement dreams come true.

Equity Compensation and Employee Stock

Employee stock plans and equity compensation often go under-utilized because of their complexity. You can maximize your earnings with an investment advisor.

Investment Planning

Your investments should empower your goals, not constantly stress you out. Diversify and optimize your investment portfolio to achieve your goals. Avoid tax implications and grow your savings with an investment advisor.

Related Reading: 3 Best Investment Strategies to Consider to Meet Your Finance Goals

Disclosure

For informational purposes only; should not be used as investment tax, legal or accounting advice. Plancorp LLC is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training nor does it imply endorsement by the SEC. All investing involves risk, including the loss of principal. Past performance does not guarantee future results. Plancorp's marketing material should not be construed by any existing or prospective client as a guarantee that they will experience a certain level of results if they engage our services, and may include lists or rankings published by magazines and other sources which are generally based exclusively on information prepared and submitted by the recognized advisor. Plancorp is a registered trademark of Plancorp LLC, registered in the U.S. Patent and Trademark Office.

![]()

![]()